Ratio analysis is one of the most widely used technique for analyzing financial statements. In this article we explore what ratio analysis is, its categories and two of the key ratios to look at- liquidity and profitability.

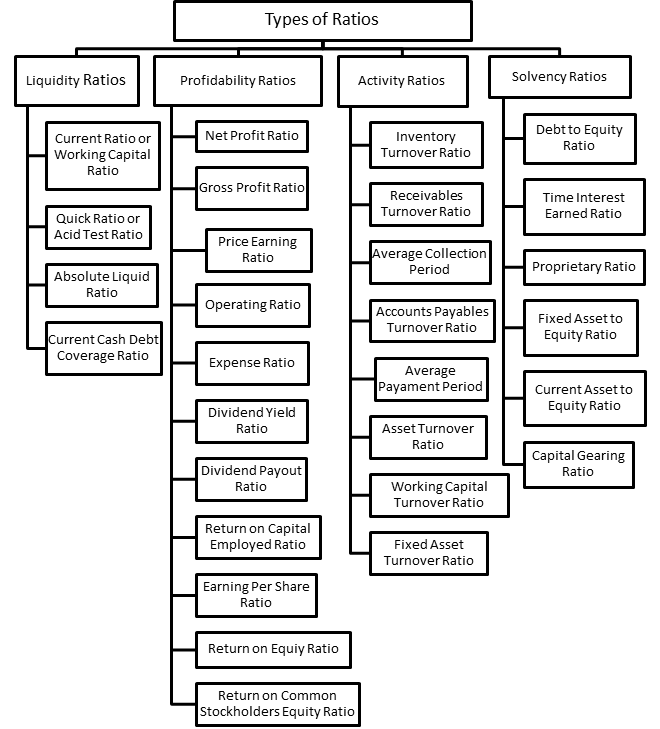

Ratio Analysis

Ratio analysis is a technical and quantitative analysis of a company’s financial statements that is used by several investors to obtain key indications about performance of the firm in several areas.

It is a tool that’s used for making comparisons across the companies within one industry or across the sector for the same company. The financial decisions of the investor are highly affected by these ratios. It facilitates the comparison of different sized firms, too. These can also be used in trend analysis to check the areas where the performance has improved or deteriorated over time.

Liquidity ratio

It is a tool to measure the adequacy of current assets, and helps to evaluate the ability of businesses to pay its short-term debt. These ratios measure the short-term solvency of the business such as maintaining sufficient current and liquid assets to pay its short-term debts is considered to have a strong solvency.

Financial Institutions and suppliers of goods or services (on credit) are often checking these ratios to estimate the solvency of the business, to check that the assets of the business are sufficient to pay its current obligations. Commercial banks and supplier might not be willing to offer loans to businesses with weak short-term solvency.

Liquid ratios are not true measures of the liquidity of the business because they only tell about the quantity of the liquid assets and not about its quality. Therefore, these should be used with care, and for a better interpretation and analysis, these should be used in combination with the activity ratios (later discussed).

Important liquid ratios are given below:

1. Current Ratio: Also known as working capital ratio, this ratio is based on items from balance sheet and it tries to compare the current and liquid assets (cash, cash equivalent, debtor) with the current obligations that are payable within a short period of time, usually a year. This ratio tells about the short-term solvency, ability to meet the current obligations of the business.

Formula: Current Ratio= Current assets/Current liabilities

2. Quick Ratio: It is one of the most important ratios to test the ability of business to meet its short-term obligations on time. It shows a relationship between the liquid asset and current liabilities present in the business.

Liquid assets: Total Current assets minus inventories and prepaid expenses.

Formula: Quick Ratio = Liquid assets/Current liabilities

3. Absolute Liquid Ratio: This ratio only considers the cash and cash equivalents for measuring the ultra- short-term liquidity of the business.

Absolute liquid Asset: Liquid assets minus accounts receivable (including bills receivables).

Formula: Absolute liquid ratio= Absolute liquid assets/Current liabilities

4. Current Cash Debt Coverage Ratio: This ratio shows a relationship between net operating cash generated over a particular period to average current liabilities (opening current liabilities + closing current liabilities)/2

It indicates the ability of the business unit to pay its current liabilities using cash generated from day-to-day business operations.

Formula: Current cash debt coverage ratio= Net cash provided by operating activities/Average current liabilities

Profitability Ratio

Profit is the key objective of all businesses. To survive and thrive, all businesses need a consistent and sufficient amount of profit over a period of time with improvements moving ahead.

These ratios help in determining the efficiency of business to use its resources in generating profit and increasing shareholder value. Almost all the parties related to a business use profitability ratios for valuation purposes and understanding the success or failure of business operations against its competitors.

A strong profitability trend ensures high dividend income and appreciation in the value of common stock holders. Management needs to ensure sufficient profit is generated to pay the dividend or to reinvest a portion in the business to increase the work capacity and improve the overall financial prospects of the business in the near future. Strong profitability also ensures the creditors and outside provider of financing safety regarding their fund and income as well as smoother running of the business.

Important profitable ratios are given below:

1. Net Profit ratio: It is a ratio between net profit after tax and net sales (denominator). The purpose of this ratio is to evaluate the profits from its primary operating activities. Higher net profit ratio indicates the efficient management of the affairs of business with better control on cost.

Net profit: Gross profit minus non-operating revenues and expenses (or Total revenue less total expense during the period

Formula: Net profit ratio= Net profit after tax/Net sales

2. Gross Profit Ratio: It is also known as ‘Gross Margin’ ratio. This ratio is used to assess the company’s financial health by diagnose the money left after accounting adjustments of Cost of Goods Sold (COGS), the core expenditure for day to day production. It disclosed the capacity of company to pay additional expenses and future savings.

Formula: Gross Profit ratio= (Revenue – COGS)/Revenue

3. Price Earnings Ratio: This is the most useful and frequently used ratio for investors, to judge the share price of the company – whether it is overvalued or undervalued in the market. This ratio enables the investor to know about his earning on per rupee of investment in the share price of a company.

Formula: Price Earnings Ratio= Market Price/Earnings per share

4. Operating Ratio: This ratio defines the operating efficiency of the management of the company; managing to reduce the expenses and generate profit of the company while revenues are decreasing. The smaller ratio is better for the company. Investors should be aware that this ratio does not include finance cost.

Formula: Operating Ratio= Operating Expense/Net Sales

5. Expense Ratio: This ratio defines the measure of costs for an investment company to operate a mutual fund. An asset management company is concerned with the operating cost and other cost incidental thereto of a mutual fund, those are taken out of a fund’s asset. It is also known as ‘management expense ratio’.

Formula: Expense ratio= Administrative and Operating Expenses/Average of Fund’s Asset

6. Dividend Yield Ratio: It comprises the per share dividend income for an investor. By using this metric, investor can analyze the return on his investment in form of dividend income compared to price paid by him/her in the market. This could be a better tool to compare two different investments on the basis of their dividend generating capacity, like equity or mutual fund.

Formula: Dividend Yield= Annual Dividend Per Share/Market Price per Share

7. Dividend Payout Ratio: It presents the percentage of net income a company is paying in the form of dividend to its shareholders. The ratio also describes the financial strength of the company and prospects for maintaining or improving its dividend payout in future. High payout ratio may not be a better indication about a company, due to the fact that the company is using less percentage of net income to reinvest in company growth. A company may decide to retain more in order to invest for business expansion in the coming period

Formula: Dividend Payout Ratio= Annual Dividend paid/Earnings per Share

8. Return on Capital Employed Ratio: This ratio indicates the operating effectiveness of the company and how efficient the company is in using its capital employed in order to generate the earnings and increase the value of shareholders’ stake. Higher the ratio, better it is for the company. It is a popular ratio used to compare two different companies under the same industry or performance of the same company for two different periods to analyze the increase or decrease in return.

Earnings before Interest and Tax: Revenue less COGS and operating expenses

Capital Employed: Total Assets less Current Liabilities

Formula: Return on Capital Employed= Earnings before interest and tax/Capital Employed

9. Earnings Per Share: It is a portion of company’s profit after dividend allocated to equity shares: allocated to the outstanding share of common stock per share. It is more accurate to use weighted average number of shares outstanding over the term, because the number of shares outstanding can different over time. It also includes ‘Diluted EPS’. Diluted EPS expands on the basic EPS by considering the expected conversions of shares of convertible or warrants outstanding in the outstanding number of shares. EPS is also the most important metric to determine the share price, by used in price-earnings ratio.

Formula: EPS= Earnings attributable to common stock/Weighted average number of outstanding common share

10. Return on Equity Ratio: This is another tool to quantify the efficiency of company in generating profits, except it only considers the equity portion of capital invested by the shareholders. It could also be used in comparison between two companies having same size of equity capital on the basis of highest ROE.

Formula: ROE= Net Income/Shareholder’s Equity

11. Return on Common Stockholders Equity Ratio: It determines the realization percentage of earnings generated by the company for common stockholders.

Stockholder’s Equity: Sum of common stock, additional paid in capital and retained earnings

Formula: Return on Common Stockholders Equity Ratio= (Net Income – Preferential dividend)/Average common stockholders’ equity

In the next part, we will look at the two other important ratios- activity and solvency.

For Annual Reports, Balance Sheets, Profit & Loss, Company Research Reports, directors and other financial information on ALL Indian Companies, head over to www.tofler.in – Business Research Platform.

Author– Harsh is a CA final aspirant with a Bachelor degree in Law. Nothing makes Harsh happier than writing on his field that can enhance his readers’ domain know-how. He loves to play with numbers and learn new things.

Editor – Anchal, co-founder at Tofler, is a CA, CS and has more than 5 years experience in company analysis. She likes to explore and track companies, their performance and senior management.